Money

WHAT TO KNOW ABOUT THE SELF-DIRECTED ROTH IRA

Are you familiar with the political compass? In 2022, who isn’t? In this familiar graphic, we see political views split into four quadrants by two axes: economic liberalism vs. conservatism on one axis, and its social counterpart on the other. Someone can be socially liberal but economically conservative, economically liberal yet socially conservative, or both of each.

Now, let’s keep the graph but put away the politics. It turns out that you can do a quadratic breakdown of individual retirement accounts, too. Let’s devote one axis to taxation: do you pay taxes on contributions or distributions? The other axis is about who calls the shots: is a custodian handling all the IRA’s transactions or is the investor involved? This yields the four most common IRAs:

- A traditional IRA, in which tax-deferred contributions fund stocks, bonds, and similar instruments,

- A Roth IRA, in which after-tax contributions fund those instruments with tax-free distributions,

- A self-directed IRA, where tax-deferred contributions can also go into unconventional investments,

- A self-directed Roth IRA, with after-tax contributions under the same looser restrictions on investments.

For some investors, this is the best of both worlds: the freedom to invest with the pleasures of tax-free income in retirement. Here’s what to know about the self-directed Roth IRA if this interests you.

Related: Really Smart Financial Moves To Make

No Self-Dealing

No matter which quadrant of our “IRA compass” you’re in, the IRS has strict prohibitions against conducting business with your own IRA’s holdings. This is a peril of self-directed IRAs both traditional and Roth, particularly when the account holds real estate.

For example, you can’t rent out your IRA’s summer cottage to family members at under market value. You may not even be able to do your own maintenance on it. While a self-directed Roth IRA is great for hands-on investors, you can’t get too hands-on.

Income and Contribution Limits

Diverse investments in a self-directed Roth IRA can grow impressively through the years, but even after taxes, contributions can’t be too large. The government designed the Roth IRA as an investment tool for the middle class, and this presumes a limit on what an investor can reasonably contribute. A self-directed Roth IRA can take up to $6,000 a year, or $7,000 over age 50. This also applies to annual income. Single filers can earn up to $140,000 a year and married people filing jointly are limited to $208,000 of total income.

Related: Inspiring Money Quotes

Your Future Is in Your Hands

What is most important to know about the self-directed Roth IRA is that you have a dizzying array of investment opportunities for a tax-free retirement. By investing in diverse avenues like cryptocurrency, debt instruments, real estate, precious metals, private businesses, and more, middle-class investors can pay Uncle Sam now and enjoy life later—when it matters most. Just be sure not to concentrate too much on one aspect.

The key to any self-directed IRA is a diversified portfolio that smooths out the bumps and glitches for an account that provides exciting opportunities with reliable returns.

With that said, before you can invest is any type of fund, you first need to have money to invest. So, start building your fortune, and then you can consider the self-directed Roth IRA as a viable investment vehicle to help you reach your investment goals.

Till next time,

STRIVE

PS – If you enjoyed found value in this post, then you’ll love this article on How to Not Work for The Rest of Your Life.

Dave Ramsey is one of the most inspiring and empowering personal finance personalities in the world. He’s been in the trenches himself when it comes money struggles, and he helps millions of people avoid some of the mistakes he’s made, and helps them overcome many of the financial challenges we all face daily. Ramsey has also authored multiple national best-selling books, and he leverages the power of radio and the internet to serve over 80 million people each and every month.

That said, when you render fortunes of service, you deserve a fortune. So, that’s exactly what we’ll be highlighting on this page, the fortune Dave Ramsey has managed to build for himself over the years. So, if you’ve want to know what Dave Ramsey’s net worth is, how much it’s grown, and how he’s managed to build it up over the years, then let’s get right into it:

What Is Dave Ramsey’s Net Worth?

Dave Ramsey’s net worth back in 2018 was around $200 million, and many other sites still show this as his current net worth to this day. However, considering his assets have been appreciating over the years, along with the growth of his business revenue, which by the way, pulled in over $300 million alone just in 2022, his net worth has grown by leaps and bounds.

In an interview with fellow financial guru, Graham Stephan, Ramsey revealed that he owns over $600 million cash in real estate.[1] In addition to this, he also revealed that he invests a good chunk of his profit every month into cash holdings that comprises of up to at least 6 months of operating capital, whereby the rest goes into investments.[2]

That said, our estimate of Dave Ramsey’s net worth for 2026 is approximately $700 million.

How Much Does Dave Ramsey Make?

This certainly begs the question with regards to how much Dave Ramsey makes a year. And while we know his enterprises gross over $300 million in revenue a year, we don’t have a precise number for how much he takes home in profits.

On the other hand, we do have a baseline income that his massive net worth could easily afford him every year. To provide this number, all we have to do is assume he’s a savvy enough investor to earn at least a 4.5% annual dividend return for the bulk of his assets (which he most likely is, considering he’s increased his net worth from 200 million to 700 million in just four short years).

We’d also have to presuppose a hypothetical selling off of all of his assets, and then transferring that money into a handful of dividend or cash paying assets like REITs, ETFs, Stocks, or Rental Property.

The result? Dave Ramsey’s annual income would easily top $31.5 million, which also comes out to about $2.6 million a month.

DAVE RAMSEY’S MONEY METRICS

| Money Metric | Amount |

|---|---|

| Net Worth: | $700,000,000 |

| **Earnings Per Year: | $31,500,000 |

| Per Month: | $2,625,000 |

| Per Week: | $605,773 |

| Per Day: | $86,539 |

| Per Hour: | $3,605 |

| Per Min: | $60.09 |

| Per Sec: | $1.00 |

Note: this is a estimated earnings metric based off the earning power of Dave Ramsey’s net worth. It does not include how much Dave Ramsey makes from projects, sponsorships, his podcast, or social media, etc. These calculations are for entertainment purposes only. Methodology

DAVE RAMSEY NET WORTH HISTORY

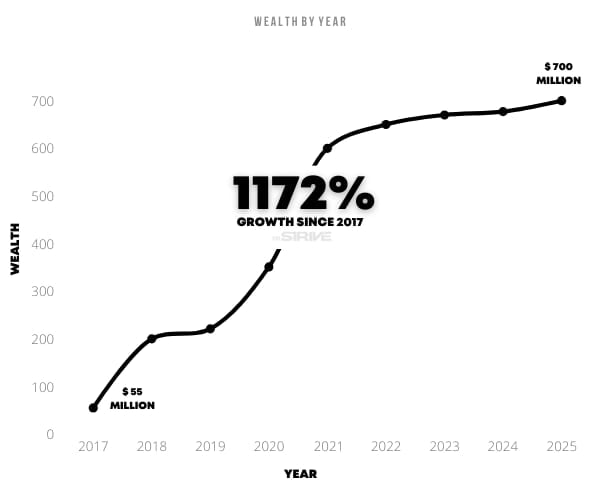

Dave Ramsey knows how to handle money, and its a big reason why he’s managed to grow his fortune from just $55 million in 2017 to the massive $700 million dollar empire he know controls.

That’s a growth rate of more than 1,172%, or a 53% year over year average! Below is a graph that highlights the impressive growth of his net worth over the years. Enjoy!

Dave Ramsey’s Social Media Influence

As Dave’s fortune has grown, so has his fame. And these days it’s never been easier to leverage your fame to make even more money with social media. That said, if you’ve ever wondered about how much extra money Dave Ramsey could make off of his social media, here’s your answer.

First things first, Dave Ramsey has 3.4 million Instagram followers, 953K Twitter followers, 5.9 million Facebook followers, 2.61 million YouTube subscribers, and 1.4 million TikTok followers. As such, his grand total of social media followers 14.2 million.

So, according to current social media marketing rates, Dave Ramsey could very easily get paid an extra $130K or so very over sponsored post he sells.

If you haven't done your taxes yet, get them over with easily by using Ramsey SmartTax!

— Dave Ramsey (@DaveRamsey) March 20, 2023

You can file confidently online with NO hidden fees. https://t.co/pKGSUu01p0

Dave Ramsey Fun Facts:

- Dave Ramsey’s show, ‘The Ramsey Show,’ is the 2nd largest radio talk show in America, with over 1 billion down loads.

- His podcast has over 80 million monthly listeners.

- Dave Ramsey’s website gets around 1.8 million visits per month.

- Dave Ramsey has published over 30 different books.

- Out of Dave’s 30+ published works, he has published 2 New York Times Best Selling Books.

- Dave Ramsey is married to Sharon Ramsey and has 3 children (Denise, Rachel, and Cruze).

- Ramsey’s business HQ consists of multiple buildings on 47 acres in Franklin, Tennessee.

- Ramsey was a multi-millionaire by the age of 26, amassing a wealth of $4 million and then losing it all at 28.[3]

How Did Dave Ramsey Get So Rich?

So, how did Ramsey get so rich? Well, Dave Ramsey has degrees in Finance and Real Estate, and he’s been involved in Real Estate since the age of 18. His parents were also involved in the Real Estate business, and were big on programming Dave’s mindset from a young age, on how to think positively, stay motivated, and get after the things he wanted.

Of course, these aren’t the only things that help Dave Ramsey get so rich. In fact, the event that has most likely allowed for Dave Ramsey to achieve so much of the success he now enjoys, has to do with his massive financial failures early in his career.

Just after he turned 28, Ramsey filed for bankruptcy. He literally lost everything financially. But, that devastating experience ended up becoming his masterclass in personal finance.

He would go on to leverage his personal experiences with gaining money and losing it, combined with the knowledge he acquired from his formal education, to create a financial coaching and consulting businesses that has been helping countless people ever since.

So, the short answer as to how Dave Ramsey has managed to get so rich is leverage. Leverage got in him into trouble initially (he was over leveraged in loans), but then learned to leverage his experiences to help people. Finally, he learned how to leverage technology/radio to reach and help more people than he ever could have had he just stuck to one-on-one consultations or seminars.

Read More: Dave Ramsey Success Story

Get Rich Like Ramsey

Now if Dave Ramsey can get rich, so can you. There’s no reason you can’t build wealth or become wealthy like Dave Ramsey has.

Sure, it may take a while, but the sooner you get started, the sooner you’ll arrive. We believe it, and so does Dave Ramsey. In fact, here are some of his very own words that say as much:

1. “Winning at money is 80 percent behavior and 20 percent head knowledge. What to do isn’t the problem; doing it is. Most of us know what to do, but we just don’t do it. If I can control the guy in the mirror, I can be skinny and rich.” – Dave Ramsey

2. “I believe that through knowledge and discipline, financial peace is possible for all of us.” – Dave Ramsey

3. “Earning a lot of money is not the key to prosperity. How you handle it is.” – Dave Ramsey

4. “You must gain control of your money or the lack of it will forever control you.” – Dave Ramsey

5. When your money makes you more than you do your are officially wealthy.” – Dave Ramsey

Read More: Dave Ramsey Quotes

More Financial Success Insights

If you’re looking for even more financial insights to help you eventually build your own massive net worth, or if you just want to know how millionaires build wealth in general, then you’ll want to watch this video below.

Brian Preston of ‘The Money Guy Show’ does a great job picking Dave’s brain on wealth-building in this extremely valuable interview.

Video Credit: The Money Guy Show (Subscribe Here)

More Insights On Building Wealth:

Key Takeaways

Here are some key Dave Ramsey takeaways:

- Dave Ramsey Net Worth: $700 million

- Annual Earnings **: $31.5 million

- Social Media Followers: 14.2 million

- Social Media Earning Power: $130K per sponsored post

- Keys to Success: Financial Education, Taking Risks, Failure, Leverage

There aren’t many other names that come to mind as quickly as Dave Ramsey’s when the topic of ‘how to be smart with your money’ comes up.

Dave’s massive net worth just goes to show how he practices what he preaches, and that he is, indeed very smart and intentional with his money.

That said, we hope we answered your questions related to Dave Ramsey’s net worth. But even more importantly, we hope we’ve inspired you to believe that you can build your own sizable fortune as well.

Till you reach those aims,

STRIVE

PS – If you enjoyed our Dave Ramsey net worth profile, then you may equally enjoy learning about the net worth of other high achievers and financial icons like the following:

Robert Kiyosaki Net Worth | Grant Cardone Net Worth | Ray Dalio Net Worth

** These earnings are hypothetical and calculated off of the earning power of Dave Ramsey’s net worth alone, assuming a 4.5% dividend yield.

Codie Sanchez is a highly successful investor, entrepreneur, speaker, and multi-millionaire who aims to help other people build wealth through contrarian thinking and investing. Having first started off in the media industry as a journalist, she switched gears to work on Wall Street and in private equity where she rapidly climbed the corporate latter and achieved a substantial level of financial success as an executive. So, that’s exactly what we’ll be highlighting on this page, Codie Sanchez’s net worth, how she managed to grow it over the years, and the earning power of her sizable current fortune.

What Is Codie Sanchez Net Worth?

First things first, Codie Sanchez is not a slow and steady type of investor. She is full of energy, and puts a lot of effort into everything she does. Just study a few of her YouTube videos, or read a few of her articles, and you’ll agree, she’s a go getter.

That said, Codie has self-disclosed that she made her first $10 million by the age of 30.[1] So, her net worth certainly requires an adjustment from her early years. Per our research and analysis, her updated net worth is indeed much higher now.

That said, after considering the $50 million business portfolio she shares with her business partner, calculating data drawn from various public sources in conjunction with the performance of the markets and the various asset classes she’s invested in over the years, Codie Sanchez’s net worth is roughly $19.47 million in 2026.

How Much Does Codie Sanchez Make?

Now that you know how much Codie Sanchez is worth, you probably want to know how much she makes. Well, we know her businesses bring in roughly $4.1 million in revenue per month, but we also know revenue isn’t profit.

Codie’s YouTube ad revenue is approximately $6.5K per month, not including the money she makes from affiliates, sponsored videos, or her masterclass. That said, it’s difficult to pin down exactly how much Codie Sanchez makes in profit from all of her current ventures. However, the profit margin for your typical small business is usually between 7 – 10%.[2]

That said, profit doesn’t always equate to how much she pays herself from these companies, but she could invest 100% back into her businesses, or 50%, or zero. We just don’t know. Of course, if we assumed Codie invested 50% (divide this by two since she’s cofounded this biz) of her profits back into her acquisitions business, and kept the difference, she could very well be banking $110K per month when you include her Ad revenue.

However, her baseline income, meaning a more cautious estimate of the amount she could easily make from her approximate net worth of $19.4 million (so long as she invested all of her money into a mix of ETFs, REITs, and stocks and followed the 4 percent rule) would be in the neighborhood of $64,900 per month.

So, Codie Sanchez could make anywhere from $64K to110K per month. The breakdown below showcases how much she could easily pull in every month without having to work another day in her life.

CODIE SANCHEZ MONEY METRICS

| Money Metric | Amount |

|---|---|

| 2024 Net Worth: | $19,470,000 |

| **Earnings Per Year: | $778,800 |

| Per Month: | $64,900 |

| Per Week: | $14,976 |

| Per Day: | $2,139 |

| Per Hour: | $89 |

| Per Min: | $1.48 |

| Per Sec: | $.024 |

Note: this is a hypothetical (but very possible) earnings Metric based off of the earning power of Codie Sanchez’s net worth alone. It does not include how much she potentially earns from projects, sponsorships, Ad revenue, or social media, etc. This calculation is an estimate and is for entertainment purposes. Methodology

Codie Sanchez Net Worth History

Codie Sanchez was on the fast track to riches, but her net worth took a big hit after she gave up 60% of her net worth (approximately $3 million) to avoid litigation.[3]

However, after her divorce she shifted gears and put herself and her finances on a completely different trajectory. This graph below showcases Codie’s net worth history by year, and according to our calculations, she’s managed to grow her fortune by approximately 289% since 2014.

Codie Sanchez Fun Facts:

- Codie Sanchez has 2.3 million Instagram followers, 561K X followers, 115K Facebook followers, 1.6 million YouTube subscribers, 1.6 million TikTok followers, 550K newsletter subscribers. As such, her social media reach is roughly 6.7 million people.

- Her YouTube channel already has over 270 million views.

- The earning power of Codie Sanchez social media reach is estimated to be approximately $30K per sponsored post.

- She graduated from ASU, has an MBA from Georgetown University, and a Ph.D. from Fundacao Gestulio Vargas.[4]

- Sanchez has aired on the following channels CNBC, Fox, CNN.

- Codie Sanchez was born in 1986 in Phoenix, AZ.

- Sanchez is currently married to a former Navy Seal.

How Did Codie Sanchez Get Rich?

Codie Sanchez is a go-getter. She started off as a journalist with The Arizona Republic while still in college, but then decided she wanted to “make money.” So, she chose to go into the industry where they “did money.”

She attended as many personal finance events as she could, and networked heavily until by happenstance she befriended a recruiter from Vanguard who helped her get her foot in the door of the industry. She then made the leap into the financial services industry right out of college.

From there, she climbed the corporate ladder, working for some of the largest financial firms in the world, working at firms like Vanguard, Goldman Sachs, and State Street. Codie spent about 2 years on average at each of those firms, starting at around $37K, then progressing to $45K, then $75K, all the way up to $250K.

Smart Money

After leaving State Street, she went and worked for First Trust for five years as Head of Latin America Investments. And again, she kept socking away her money into the market the whole time.

But, after a few years of crushing it in the cut-throat industry of traditional finance, Codie Sanchez finally decided to walk away. So, she’s switched gears and chose to become a private equity investor in cannabis.

After hustling for nearly three years at one of the first growth equity firms in the cannabis industry, she co-founded Unconventional Acquisitions, while launching her Contrarian Thinking media business at virtually the same time.

That said, despite all the different companies Codie was working for, she was smart with her money, and she saved large chunks of her earnings the whole time she was employed. It’s important to note that she didn’t just save her money, she put it to work for her in the stock market and other high return investments.

Which, over time, earned her millions of dollars. Compound interest plus choosing wise investments skyrocketed her wealth.

So, how did Codie get so rich? The good old fashioned way. She worked hard to rise to positions that paid well, and she channeled large chunks of her earnings into assets that compounded and appreciated over time.

Codie Sanchez Success Insights

That said, Codie shares a lot of her own insights on how to find success and build wealth on her YouTube channel, blog, and newsletter. So, we decided to capture some of her best advice and takes on what leads to financial success via the Codie Sanchez quotes below:

1. “Your earned salary will be your biggest driver to wealth to begin with.” – Codie Sanchez

2. “If you do what the average person does, you will be as the average person is. Average.” – Codie Sanchez

3. “Everybody wants the hack. Be the person who does the work.” – Codie Sanchez

4. “You have to be the architect of your own life. The biggest mistake you can make is let somebody else write your story.” – Codie Sanchez

5. “Patience Tips: 1. Save More Than You Spend. 2. Invest Your Savings. 3. Compound Those Savings.” – Codie Sanchez

Read More: Millionaire Quotes

Extra Success Insights

If you’re looking for even more insights about how Codie built her wealth, she lays out some invaluable insights in this short video. If you have a few minutes give it a watch, as she provides a great lesson on the power of dreaming big, starting small, and building up.

Video Credit: Codie Sanchez (Subscribe Here)

Related Wealth Building Resources:

- How To Build Your Net Worth

- 5 ETFs That Can Make You Rich

- How To Become a Millionaire

- Key Financial Statistics

Key Takeaways

Here are some key Codie Sanchez takeaways:

- Codie Sanchez Net Worth: $19.5 million (rounded up)

- Annual Earnings **: $51 million

- Social Media Followers: 6.7 million

- Social Media Earning Power: approximately $30K per sponsored post

- Keys to Success: Hard Work, Strategic Job Hopping, Contrarian Investing

Codie Sanchez’s massive net worth seems to be directly related to her action-oriented personality, the disciplined investment of her early income, and her ability to take risks on investments that most people overlook.

Considering she’s constantly creating, innovating, and buying new businesses, we don’t doubt that her fortune will continue to grow over the years, so stay tuned.

Also, if you enjoyed this Codie Sanchez net worth profile, then you may equally enjoy learning about the net worth of other high achievers and influencers like:

Tom Bilyeu New Worth | Alex Hormozi Net Worth | Pace Morby Net Worth

That said, we hope you enjoyed this write up, if it inspired you or even entertained you, please do us a favor and share it with someone who may benefit from Codie’s inspiring story and wealth building insights.

Till you reach your aims,

STRIVE

** All of these figures are estimates and are calculated off of the earning power of Codie Sanchez’s approximate net worth assuming a 4.0% dividend yield.

Sylvester Stallone earned worldwide recognition as an actor, screenwriter, and director after starring in his own screenplay for the movie ‘Rocky’, which would go on to win an academy award for Best Picture. After starring in this hit movie, Stallone’s career and earnings would skyrocket over the years, especially after creating five ‘Rocky’ sequels, and classics like ‘Rambo I, II, and II’, Over the Top, ‘Demolition Man’ and many more.

Now with over 75 films under his belt, and with all of them producing over $4 billion in revenue, Stallone has amassed a small fortune. In fact, many people commonly ask if Sylvester Stallone is a billionaire due to how much his films have produced. However, the answer is no, he is not a billionaire. But, that’s exactly what we’ll be highlighting on this Sylvester Stallone net worth page; the size of his fortune and his current earning power.

What is Sylvester Stallone’s Net Worth?

So how big of a fortune has Sylvester Stallone amassed? Well according to a variety of online sources, Sylvester Stallone’s net worth was approximately $400 million. However, our research shows that those estimates are outdated, considering many sites have had the same estimate up since 2021.

Considering the fact, here’s something to think about. If all of Stallone’s $400 million dollar fortune was invested into an index fund like the SP500 back in 2021, his net worth would be worth nearly $542.8 million today.

With that said, we’ve considered the fact that real estate markets grew by around 19% in 2021 and were flat in 2022 and 2023, with a slight up tic in 2024, and a steady 2025. In addition to that, we also incorporated how the markets have on average increased by about 31 % over the past three years, to give us safe and very conservative estimate for Stallone’s updated net worth.

So with a modest 7 – 10% growth over the past few years, and knowing that Stallone has around 14% of his net worth tied up into real estate, it’s safe to say that Sylvester Stallone’s Net Worth for 2026 is approximately $450 million.

How Much Does Sylvester Stallone Make?

At the height of Stallone’s career, he was making between $15 million to $25 million per movie, and was named Hollywood’s highest paid actor. His highest earning year on record was 1994 at $60 million.[1] As of late however, his movies have not made nearly as much money as he made in his prime. In addition, there has been minimal publication of his recent earnings, aside from the $3 million dollars hear earned for his role in The Suicide Squad.

However, even without those numbers, will still aim to provide you with Stallone’s money metrics based off his net worth of $450 million alone. It will be hypothetical, but a fun metric to consider based off of his Net Worth’s earning power alone.

Therefore, all we have to do is assume Stallone leverages the 4 percent rule, and earns himself a 4% annual dividend yield on his combined $450 million net worth, by investing it in a handful of historically strong investments like stokcs, ETFs, REITS, etc. If he did this, his annual earnings would easily come out to $18 million without including any other sources of income.

FYI a 4.0% yield is more than a reasonable return to expect, especially considering historical returns on safe investments in the past yielded between a range of 3% to 5% range. [2]

Sylvester Stallone’s Money Metrics

| Money Metric | Amount |

|---|---|

| Net Worth: | $450,000,000 |

| Earnings Per Year: | $18,000,000 |

| Per Month: | $1,500,000 |

| Per Week: | $ 346,154 |

| Per Day: | $49,450 |

| Per Hour: | $2,060 |

| Per Min: | $34.34 |

| Per Sec: | $0.57 |

Disclaimer: This is an estimated earnings metric based off of the earning power of Sylvester Stallone’s net worth alone. As mentioned earlier, it does not include how much he potentially earns from projects, sponsorships, or social media he’s earned this year. Again, this calculation is for entertainment purposes only. Methodology

Social Media Influence

Stallone’s social media influence has continually grown over the years, despite the slowdown in blockbuster releases. That said, he currently has around 15.9 million Instagram followers, 11 million Facebook Followers, and 2.9 million Twitter followers. This comes out to a grand total of 29.8 million social media followers.

So, in the event Stallone wanted to take advantage of his social media influence, he could potentially negotiate roughly $250K per sponsored post. That’s not a bad payout for a social media side hustle.

Remember you are NEVER to old to stop Punching! https://t.co/zBBXccKhbd

— Sylvester Stallone (@TheSlyStallone) January 7, 2023

Stallone’s Key Facts

- Stallone’s signature snarled lip was due to an injury at birth by the forceps which grabbed his face, leading to the severing of some of the nerves of his lips and eyelid.

- In his youth, he was kicked out of school over 14 times.

- He attended college in Switzerland.

- Before Sylvester Stallone hit it big, he briefly experienced homelessness, where he spent a few nights sleeping on the floor of a bus station.

- Sylvester Stallone once hired two-time Mr. Olympia Franco Columbo as his personal trainer.

- Stallone has earned more “worst actor” awards than any other in Hollywood.

- He owns an $18.2 million dollar home in Hidden Hills, CA, and a $35 million dollar home in Palm Beach, FL.

How Did Sylvester Stallone Become So Successful?

Sylvester Stallone has a wonderfully inspiring success story, and you can read an in depth account of it here. However, here is a short version of how Stallone became so successful. In essence, Stallone pursued his dream of becoming a successful actor for many years.

He suffered through working menial jobs, taking on low budget films, and pretty much doing whatever he could to make ends meet while pursuing an acting career on the side. Stallone embodied the concept of hustle, before hustling was a thing.

As such, his success ultimately stemmed from failing over and over again, and persisting long enough till he found his break. A break which he finally received after pitching the idea of what would come to be the ‘Rocky’ film to two movie producers he met during a casting call.

It was a massive opportunity that he seized, and reaped the benefits for stardom to go on to create, star in, and produce many more films through out his career.

So, how Stallone became so successful can be summed up to… persisting in the face of failure.

And he’s still going strong! Still swinging!

Video Credit: The Richest – (Subscribe to Their Channel Here)

Build Your Net Worth Like Stallone

Sylvester Stallone’s accomplishments are impressive, and have helped him build such a large net worth. But, as the saying goes, it’s not about how much you make, it’s about how much you keep (of course, making millions does help).

With that being said, if you want to know how you can go about increasing your own net worth like Sly Stallone, here’s a few solid resources to get you started:

Key Takeaways

Here are some key Sylvester Stallone takeaways:

- Sylvester Stallone Net Worth: $450 million

- Annual Earnings **: $18 million

- Social Media Followers: 29.8 million

- Social Media Earning Power: $250K per sponsored post

- Keys to Success: Persistence

The biproduct of getting back up each time he got knocked down is the building of a massive net worth. To be sure, Stallone’s success and sizeable fortune is a direct result of his not quitting when the going got tough, and sticking to his plans and dreams until they manifested themselves.

With that being said, we hope you take these insights and use them to keep moving forward towards achieving your dreams and growing your bank account.

And never forget… the major difference between the big shot and the little shot is – the big shot is just a little shot who kept on swinging.

Till next time,

STRIVE

PS – If you enjoyed this Sylvester Stallone Net Worth page, then chances are you’ll enjoy these net worth profiles:

Arnold Schwarzenegger Net Worth | Robert Downey Jr. Net Worth | Will Smith Net Worth

Feel free to take a look at our collection of Net Worth profiles on other notable successful people and high achievers as well.

** These earnings are hypothetical and calculated off the earning power of Sylvester Stallone’s net worth alone, assuming a 4.0% dividend yield.

Barbara Corcoran’s net worth as of 2026 is approximately $150 million. If you’re not familiar with Barbara, she’s a highly successful businesswoman, investor, and television personality, who is best known from her appearances on the wildly popular reality show ‘Shark Tank’. She’s also the founder of The Corcoran Group, Shark, and is the Executive Producer of ABC’s “Shark Tank”.

Having once turned $1,000 into a multi-billion dollar business, she’s managed to build up an impressive fortune for herself in the process. That said, if you’re interested the earning power of Barbara Corcoran’s net worth, how much her net worth has changed over the years, and exactly how she became so rich, let’s get into it:

Barbara Corcoran Net Worth Details

Barbara Corcoran’s Net Worth was estimated at $100 million back early 2020. However, per our research and analysis, her updated net worth is much higher now. As a savvy investor, she should be able to beat the market, but we have a hunch capital preservation is key since she’s already amassed her fortune.

Here’s an interesting fact, if Barbara’s entire $100 million fortune were invested into the SP500 back in 2020, it would now be worth $185 million. And that’s without her even adding one single dime to it.

That said, after calculating data drawn from various public sources in conjunction with the performance of the markets and various asset classes she’s invested in, Barbara Corcoran’s net worth is approximately $150 million in 2026.

How Much Does Barbara Corcoran Make Per Year?

This certainly begs the question with regards to how much Barbara Corcoran makes a year. With it estimated that she get’s paid $500,000 per Shark Tank appearance (which is likely higher than the other sharks because she’s the Executive Producer), she’s makes on average $6.5 million per year from the show alone. She also makes money from book royalties, and her various investments in startup businesses, and from charging between $100K – $200K for her speaking events.[1]

Addition to this, the earning power of her net worth alone (presupposing she follows the 4 percent rule) comes out to $6 million per year. As such, Barbara Corcoran makes roughly $14.5 million per year.

Here’s how that breakdowns:

BARBARA CORCORAN MONEY METRICS

| Money Metric | Amount |

|---|---|

| Net Worth: | $150,000,000 |

| **Earnings Per Year: | $14,500,000 |

| Per Month: | $1,208,333 |

| Per Week: | $278,848 |

| Per Day: | $39,835 |

| Per Hour: | $1,659 |

| Per Min: | $27.7 |

| Per Sec: | $.46 |

Note: This is an estimated earnings metric based off the earning power of Barbara Corcoran’s net worth and income estimations. We apply our own rigorous methodology to supply you with accurate calculations; however, these figures are ultimately for informational and entertainment purposes only. Methodology

Barbara Corcoran’s Net Worth History

Barbara has been growing her wealth for years now since hitting it big with her first big pay out. That said, per our research, her wealth has grown by an impressive 275% since 2014. Which means, her year over year growth since 2014 is approximately 15%.

Here’s what her Net Worth history looks like graphed:

Barbara Corcoran Fun Facts:

- Barbara Corcoran has 867K Instagram followers, 739K Twitter followers, 544 K Facebook followers, and 9.8K YouTube subscribers. As such, her grand total of social media followers is 2.16 million.

- She got straight D’s in high school and college.

- Held 20 different jobs by the time she turned 23.

- She founded what would become a thriving real estate business for $1,000.

- Barbara’s favorite drink is a mojito.

- Barbara Corcoran’s husband is an ex FBI agent, and a retired Navy captain.

- She’s was once a teacher, and has published at least four different books.

How Did Barbara Corcoran Get So Rich?

This is how Barbara Corcoran got so rich; in 1973 she opened up her own real estate firm in New York city, called the Corcoran Group. The company slowly but steadily became a prominent real estate brokerage with a strong brand and presence in New York and across the country.

After 28 years of empire building, Corcoran finally decided to sell the company. As such, she sold her company to real estate giant NRT for $66 million.[2]

So, in a nutshell, the bulk of Barbara Corcoran’s riches stems from hustling for nearly three decades to build a solid reputation and high-quality brand in the real estate industry, and then off-loading that asset to an interested buyer.

Related: Barbara Corcoran Success Story

In Her Own Words

Here are a few powerful Barbara Corcoran quotes that highlight the mindset that has helped her become one of the richest and most well-known female investors in the world:

1. “My best successes came on the heels of failure.” – Barbara Corcoran

2. “Stop putting it off! Procrastination breeds guilt, guild breeds depression, and depression breeds failure.” – Barbara Corcoran

3. “You don’t need an MBA to launch a business. You need street smarts and grit.” – Barbara Corcoran

4. “The hardest lesson to learn is that you are more capable than you think you are.” – Barbara Corcoran

5. “You don’t have to get it right, you just have to get it going.” – Barbara Corcoran

Related: Barbara Corcoran Quotes

Extra Success Insights

That said, a few additional insights about what drove Barbara Corcoran to become so rich and successful can be gathered from this video. It’s a short video where she was interviewed by ‘Now This’, but it reveals a lot of what fueled her desire to achieve, as well as her take on what ultimately led to her success and wealth.

Give it watch, it’s worth every minute:

Video Credit: Now This News (Subscribe Here)

Related Wealth Building Resources:

Key Takeaways

Here are some key Barbara Corcoran takeaways:

- Barbara Corcoran Net Worth: $150 million

- Annual Earnings **: $14.5 million

- Asset Earnings**: $6 million

- Social Media Followers: 2.16 million

- Social Media Earning Power: approximately $20K per featured post

- Keys to Success: Intention, Hard Work, Over Preparation, Taking Action

Barbara Corcoran’s massive net worth is the result of decades of hard work, dogged persistence, and having the business acumen to know when to cash out. Her story is one we could all learn and benefit from.

That said, we hope you got what you were looking for as it relates to the net worth of Barbara Corcoran, how much she makes, and how she made it. If you enjoyed our page, please share it or come back when you’re in need of a bit of inspiration or insight for building wealth.

Till you reach your financial aims,

STRIVE

PS – If you enjoyed our Barbara Corcoran net worth profile, then you may equally enjoy learning about the net worth of some of her fellow sharks, like Kevin O’Leary, Mark Cuban, or Daymond John.

** These earnings are hypothetical and calculated off of Barbara Corcoran’s net worth’s earning power alone assuming a 4.0% dividend yield.

Ray Kroc was the iconic American businessman who transformed McDonalds into a global multinational fast food chain, and lead it to become not only the most popular fast food chain in the world, but also the most successful. After spending nearly two decades at the helm of the corporation, he created the company’s legacy and generated a fortune for himself in the process? How big of a fortune? Well, that’s exactly what we aim to highlight in this Ray Kroc net worth write up.

So, if you’ve ever wanted to know what Ray Kroc’s net worth was at the time of his death, what it would be worth today, and how he specifically built his fortune, then this page is for you. Let’s dive into the details:

What Was Ray Kroc’s Net Worth?

At the time of Ray Kroc’s death in 1984 his net worth was approximately $600 million. Which is a lot of money even by today’s standards.

That said, if we adjusted for inflation all the way up to 2026, Ray Kroc’s net worth today would be closer to $1.8 billion. So, Ray Kroc was technically a billionaire. And there’s little doubt that if he were alive today (assuming his fortune wasn’t given away to charity), he would be a multibillionaire.

How Much Did Ray Kroc Make Per Year?

There are little to no reliable records of Ray Kroc’s income or salary at the time of his death. That said, we can provide you with an estimated income based off of the earning power of what Ray Kroc’s net worth is today.

As such, this figure assumes Ray Kroc’s modern-day fortune would be allocated into a basket of dividend paying stocks, ETFs, or REITs that earn a modest 4% annual yield minimally. So, if we were to make such an assumption, Ray Kroc’s yearly passive income by today’s standards would come out to roughly $73 million per year.

And this is a conservative estimate, meaning he could have easily earned much more if he placed his money in more aggressive investments.

RAY KROC’S MONEY METRICS

| Money Metric | Amount |

|---|---|

| Net Worth: | $ 1,830,000,000 |

| **Earnings Per Year: | $73,200,000 |

| Per Month: | $6,100,000 |

| Per Week: | $1,407,692 |

| Per Day: | $201,098 |

| Per Hour: | $8,379 |

| Per Min: | $139 |

| Per Sec: | $2.32 |

Note: this is a hypothetical (but very possible) earnings metric based off the estimated earning power of Ray Kroc’s net worth today. It does not include how much Ray Kroc made his salary, or the royalties and dividends received from ownership of McDonalds. This calculation is for entertainment purposes only. Methodology

Key Ray Kroc Facts:

- Ray Kroc was born in Oak Park, Illinois in 1902.

- Ray Kroc died in San Diego, Californio in 1984.

- Kroc wasn’t the founder of McDonalds.

- Kroc acquired McDonalds in 1954.

- Ray Kroc purchased the San Diego Padres in 1974.

- Kroc suffered from alcoholism.

- Ray Kroc was married three different times and had 1 child.

How Did Ray Kroc Get Rich?

Ray Kroc worked in a variety of different industries before he hit it big. He was once a musician, a real estate salesman, a paper cup salesman, and then eventually a milkshake machine salesman.

Every job he had helped him acquire knowledge and skills that would later help him grow and scale his future operations in the fast-food industry. That said, Kroc was nearly 52 years old when he finally caught his big break.

In 1954 while working as a milkshake salesman, Kroc stumbled upon the McDonald’s restaurant. He instantly realized the potential of the business due to the demand for simple (hamburgers, fries, and milkshakes) yet delicious food, and the automation process that the McDonald’s brothers were using to meet that demand.

Kroc partnered with the two bothers and focused on franchising the brand and it’s assembly line operations to interested owners. The idea to do so was a success and it was extremely profitable.

Ray Kroc’s knack for selling paid off, as he sold the idea of franchising owners all across the country. By 1959 he hit 100 restaurants, and two years later in 1961 it was at 228.

Just 7 years after coming across the McDonald brother’s operations, Ray Kroc would buy them out for a mere $2.7 million (approximately $27 million by today’s standards).[1]

13 years later, Ray Kroc would eventually retire as the CEO of the company, but he remained involved as chairman until his death. While still alive, his hamburger empire grew to over 7,500 different franchises all across the world.

So, how did Ray Kroc get rich? Here’s how in three words, systems, selling, and scaling.

Extra Success Insights

That said, here a few powerful words and success anecdotes that give additional insight into the type of thinking that helped Ray Kroc achieve so much success and riches in his lifetime:

1. “The More I Help Others Succeed, The More I Succeed.” – Ray Kroc

2. “To Be Successful, You Must Be Daring, Be First And Be Different.” – Ray Kroc

3. “If You Believe In It, And You Believe In It Hard, It Is Impossible To Fail.” – Ray Kroc

4. “The Key To Success Is To Focus On Your Goals, Not Your Obstacles.” – Ray Kroc

5. “Luck Is A Dividend Of Sweat. The More You Sweat, The Luckier You Get.” – Ray Kroc

If you’re looking for even more insights into how Ray Kroc built his fast-food empire and achieved his fortune, then give this video a watch. It does a good job outlining the history of The McDonald’s brother’s startup, and how Ray Kroc seized opportunity and snatched it up:

Video Credit: Jake Tran (Subscribe Here)

Related Resources on Wealth Building:

Key Takeaways

Here are some key Ray Kroc takeaways:

- Ray Kroc Net Worth: $1.83 billion

- Annual Earnings **: $73 million

- Keys to Success: Sales, Systems, Scaling Up

Ray Kroc’s massive net worth is directly related to the number of people he’s served. Not only did he provide invaluable service to hundreds of millions of people by way of fast and convenient food; but he also helped create hundreds of millionaires through the franchising of their own McDonald’s business.

That said, if you enjoyed this Ray Kroc net worth profile, then you may equally enjoy learning about the profiles of entrepreneurs who built business empires on par with Ray Kroc’s:

Walt Disney Net Worth | Richard Branson Net Worth | Colonel Sanders Story

If we successfully provided you with the Ray Kroc net worth details you were looking for and more, please share the page and come back soon.

Till you reach your financial aims,

STRIVE

** These earnings are hypothetical and calculated off the earning power of Ray Kroc net worth today assuming a 4.0% dividend yield.

Lewis Howes is a highly successful entrepreneur, peak performance coach, podcast host, and inspirational best-selling author. He’s best known for his award-winning and highly popular podcast ‘School of Greatness’, where he interviews high achievers, celebrities, and success icons from all over the world. He’s been at it since 2013, and has accrued a sizable fortune as an influencer, marketer, and master networker. How sizeable? Well, that’s exactly what we aim to highlight in this Lewis Howes net worth profile.

So, if you’ve ever wanted to know what Lewis Howes’ net worth is, how he built it, and how much he likely makes from these days, then let’s dive into this page:

What Is Lewis Howes’ Net Worth?

Per our research, most of the major net worth profile sites have outdated information on Lewis Howes’ net worth. In fact, most showcase data that hasn’t been updated since 2016.

That said, we’ve conducted our own net worth analysis for Lewis Howes using updated information and market data. So, per our analysis, Lewis Howes net worth as of 2026 is approximately $17 million.

How Much Does Lewis Howes Make Per Year?

In 2012, Lewis Howes made $2.5 million in revenue just from his webinar business.[1] Then he founded his podcast in 2013, and his income trend didn’t stop.

Given that his podcast has acquired over 500 million downloads so far, we can estimate that he’s made over $25 million from his podcast alone since launching it. This comes out to an average of $2.5 million per year from advertisers and affiliates alone.[2]

He also makes money through books sales and speaking engagements, which is estimated to at approximately $250K per year. And assuming Lewis Howes is a savvy investor, he likely earns money every year just from his money.

Therefore, presupposing Lewis Howes is a savvy enough investor to earn an annual 4% yield on his combined $17 million net worth (4% is a reasonable minimum annual yield to expect on investments considering historical returns on safe investments have typically fallen between the 3% to 5% range annually), he likely brings in an additional $680K a year just from his financial assets.

When you add it all up, Lewis Howes makes roughly $3.4 million per year.

LEWIS HOWES MONEY METRICS

| Money Metric | Amount |

|---|---|

| Net Worth: | $17,000,000 |

| **Earnings Per Year: | $3,430,000 |

| Per Month: | $285,833 |

| Per Week: | $65,961 |

| Per Day: | $9,423 |

| Per Hour: | $392 |

| Per Min: | $6.54 |

| Per Sec: | $.10 |

Note: this is an estimated earnings Metric based off the earning power of Lewis Howes estimated net worth along with his estimated earnings from book royalties, advertisers, and other business dealings. This calculation for entertainment purposes only. Methodology

Lewis Howes’ Social Media Earning Power

One thing we didn’t include in Lewis Howes’ monthly/yearly income, was the potential income he makes from social media. Because it’s difficult to assess how many sponsored posts Lewis Howes does per year, we’ll just give you how much his social media earning power is per post.

First things first, here are his social media numbers. Lewis Howes has 3.1 million Instagram followers, 247K X followers, 2.9 million Facebook followers, 1.9 million TikTok followers, and 3.13 million YouTube subscribers. As such, the grand total of his social media followers is 11.3 million.

That said, per current social media market rates with all the social media platforms combined; Lewis Howes’s social media earning power is roughly $57K per sponsored post.

How Did Lewis Howes Get Rich?

Lewis Howes played semi-pro football after college. Unfortunately, his football career abruptly ended after a hand injury.

In short order he found himself living on his sister’s couch, struggling to make ends meet. After deciding to move out to New York to play handball, Howes began leveraging LinkedIn for networking purposes in the sports industry, and to make some enough money so he could move there.

Howes was given some good advice to get on Linked by mentor of his. So, he created a LinkedIn Groups page and successfully built one that attracted a lot of attention.

He leveraged his newfound skillset to coach other people on how to land jobs and use Linkedin to improve their business and professional goals.

Soon after, Howes transformed what he knew about Linkedin into a multimillion-dollar education business that specifically taught people in the sports industry how to leverage Linkedin and find jobs in sports.

Howes then went on to create a podcast that allowed him to branch out to new leaders in all walks of life. He would go on to interview leaders and success icons from all over the world, extracting and sharing their success secrets so that others could learn how to create a business and lifestyle they were excited about.

And as they say, the rest was history. Lewis Howes’ podcast would go on to become a massive success, earning him over 8 figures since launch, and allowing him to then leverage it for even more business opportunities.

Key Takeaways

Here are some key Lewis Howes takeaways:

- Lewis Howes Net Worth: $17 million

- Annual Earnings **: $3.4 million

- Social Media Followers: 11.3 million

- Social Media Earning Power: $57K per sponsored deal

- Keys to Success: Networking, Leveraging Technology, Branding

Lewis Howes has created a sizeable net worth and strong brand in a relatively short amount of time. To this day he continues to expand his network, leverage technologies, and help people all across the world with his podcast, YouTube show, and as a high-performance coach.

So, we can expect his success, fame, and fortune to grow for years to come. That said, if you enjoyed this Lewis Howes net worth profile, then you may also enjoy these related profiles:

Mel Robbins Net Worth | Ed Mylett Net Worth | Jay Shetty Net Worth

Till you reach your aims,

STRIVE

** These earnings are hypothetical and calculated off of the earning power of Lewis Howes’ net worth alone assuming a 4.0% dividend yield.

Paulo Coelho is the author of one of the most inspiring best-selling books of all-time, ‘The Alchemist’. In addition to that book, he’s also authored 32 other books. Coelho has already sold over 350 million copies of ‘The Alchemist’ alone, and his sales continue to grow. As such he ranks in the top 25 for most books sold and is considered one of the richest authors in the world. How rich? Well, that’s exactly what we aim to highlight in this Paulo Coelho net worth profile.

Having said that, if you’ve ever wanted to know exactly how much money Paulo Coelho has managed to keep as one of the most prodigious authors in modern times, then this page is for you. We’ll also touch on how much his net worth could afford him in terms of an annual passive income.

What Is Paulo Coelho’s Net Worth?

As of 2026 Paulo Coelho’s net worth is approximately $570 million. Coelho’s vast net worth primarily stems from the hundreds of millions of books he’s sold over the past four decades.

He’s owned property in places like Rio de Janeiro, Brazil, The Pyrenees in France, and Geneva, Switzerland, and has the rest of his money tied up in savings, stocks, and other assets.

How Much Does Paulo Coelho Make Per Year?

Paulo Coelho’s biggest paychecks have come from his book royalties, but he may also bring in extra money from paid speeches, and allowing his material to be used in movies and T.V. series.

That said, there’s little to no publicly verifiable data on how much Paulo Coelho makes a year, aside from calculating his royalties from books sole each year, but that data is private until it isn’t. But here’s what we know he could earn based off of his net worth alone.

Assuming Coelho invested the bulk his money in safe assets with an annual yield of at least 4%, he could very easily make $22.8 million a year in passive income (for perspective, 4% is a reasonable minimum annual yield to expect on investments considering historical returns on safe investments have typically fallen between the 3% to 5% range annually).

PAULO COELHO MONEY METRICS

| Money Metric | Amount |

|---|---|

| Net Worth: | $570,000,000 |

| **Earnings Per Year: | $22,800,000 |

| Per Month: | $1,900,000 |

| Per Week: | $438,461 |

| Per Day: | $62,637 |

| Per Hour: | $2,609 |

| Per Min: | $43.5 |

| Per Sec: | $.72 |

Note: this is a hypothetical (but very possible) earnings metric based off the earning power of Paulo Coelho’s net worth. It does not include how much Paulo Coelho makes from ongoing projects, sponsorships, royalties, etc… This calculation is for entertainment purposes only. Methodology

Paulo Coelho’s Social Media Earning Power

Have you ever wondered what Paulo Coelho’s social media influence was worth? If so, we’ve pulled together his social media reach to give you an estimate of how much he could charge for each sponsored social media post.

First things first, here is Paulo Coelho’s social media reach: He currently has has 30 million Facebook followers, 15 million Twitter followers, 2.3 million Instagram followers, and 474K YouTube subscribers. As such, his grand total of social media followers 47.7 million.

As such, Paulo Coelho’s massive reach on social media could give him the ability to demand roughly $350K per sponsored post.

Key Paulo Coelho Facts:

- Paulo Coelho once worked as a song writer.

- Paulo Coelho was born in Rio de Janeiro in 1947.

- Coelho didn’t become a millionaire until he was well into his 40s – so never say its too late.

- He is now one of the richest writers in the world.

How Did Paulo Coelho Get Rich?

Paulo Coelho initially gave up his dream to become a lawyer. It wasn’t what he wanted to do, but his parents nudge him in that direction.

Eventually Coelho dropped out and lived a nomadic lifestyle for a while. After he got the travelling out of his system, he moved back to Brazil and made money as a song writer.

He also acted, directed theater, and even made money as a journalist to get by. But Paulo Coelho eventually got rich by following his dream of becoming a writer.

Read More: Paulo Coelho Story of Success

In 1982 in his mid thirties he began publishing books. But it wasn’t until he wrote ‘The Alchemist’ that his financial situation would dramatically shift.

His luck didn’t change overnight in 1988 when he published ‘The Alchemist’, but through persistence and belief in his work, his masterpiece eventually picked up steam.

And every year since publishing the book, his sales would grow larger and larger, and after only 10 short years he hit the 100 million sales mark. So how did Paulo Coelho get rich? Sales, book sales… millions upon millions of them.

Related Wealth Building Resources:

Success Insights

That said, here a few powerful words and success anecdotes that Paulo Coelho has uttered himself over the years that may just help you gain a better understanding about how he did it:

1. “You are what you believe yourself to be.” – Paulo Coelho

2. “When you want something, all the universe conspires in helping you to achieve it.” – Paulo Coelho

3. “When you want something, all the universe conspires in helping you to achieve it.” – Paulo Coelho

4. “It’s only those who are persistent and willing to study things deeply, who achieve the master work.” – Paulo Coelho

5. “Be brave. Take risks. Nothing can substitute experience.” – Paulo Coelho

6. “There is only one thing that makes a dream impossible to achieve: the fear of failure.” – Paulo Coelho

7. “If you don’t care about what people think, you already passed the first step of success.” – Paulo Coelho

Related: Paulo Coelho Quotes

Key Takeaways

Here are some key Paulo Coelho takeaways:

- Paulo Coelho Net Worth: $570 million

- Annual Earnings **: $22.8 million

- Social Media Followers: 47.7 million

- Social Media Earning Power: Roughly $350K per sponsored post

- Keys to Success: Taking Risks, Following His Dreams, Writing Well

Paulo Coelho’s journey to riches is truly an inspiring one. There’s no doubt that his net worth is extraordinary, and that the method of achieving his riches is not typical.

That said, who knows what’s possible when you listen to your heart and chase your dreams and not the money.

One last thing, if you enjoyed our Paulo Coelho net worth profile, then you may equally enjoy learning about the net worth of other writers and artists like the following:

Sylvester Stallone Net Worth | Walt Disney Net Worth | Steven Spielberg Net Worth

Till you reach your aims,

STRIVE

** These earnings are hypothetical and calculated off of the earning power of x’s net worth alone assuming a 4.0% dividend yield.

YOUR DAILY MOTIVATIONAL QUOTE TO KEEP YOU INSPIRED

DAVE RAMSEY’S NET WORTH AND HOW HE BECAME SO RICH

CODIE SANCHEZ NET WORTH AND HOW SHE BUILT HER FORTUNE

SYLVESTER STALLONE’S NET WORTH AND HOW HE GOT SO RICH

BARBARA CORCORAN NET WORTH + HOW SHE GOT SO RICH

RAY KROC’S NET WORTH + HOW HE BUILT HIS FORTUNE

LEWIS HOWES NET WORTH AND HOW HE GOT SO RICH

15+ BEST BOOKS TO BUILD SELF-DISCIPLINE AND SELF-CONTROL (2026)

NO GUTS, NO GLORY QUOTES

GET FIRED UP: 365 MOTIVATIONAL QUOTES TO KEEP YOU MOTIVATED DAILY

GRANT CARDONE’S NET WORTH AND HOW HE GOT SO RICH

10 WAYS TO ACHIEVE YOUR GOALS IN 2026

ELON MUSK NET WORTH AND HOW HE GOT SO RIDICULOUSLY RICH